Cost Breakdown & Should-Cost : Negotiate with facts (not opinions)

Should-cost analysis separates buyers who accept price hikes from category managers who control them. The complete method — how to build, use, and defend it.

On this page

- What is Cost Breakdown?

- The 7 standard items

- Should-Cost : the next level

- The 3 levels of maturity

- Method for products

- Method for services

- The typical breakdown of a service

- Concrete example: outsourced call center

- Where to find the data

- In negotiation : two approaches, two contexts

- Classic mistakes (and how to avoid them)

- Cost Breakdown's place in your complete toolkit

- In summary

- Next article in the series

Series · Tool #5 of 6 · Phase 2 — Tactical Execution

Cost Breakdown & Should-Cost : Negotiate with facts (not opinions)

The difference between a buyer who suffers price increases and a category manager who contests them — this is that tool.

● 12 min read● Tool #5 — Cost Breakdown● Level : Intermediate → Expert

A lived, universal scene. You're in a negotiation. The supplier puts their cards on the table: +14% increase on the next contract. You say it's too much. He says it's inevitable. You cite inflation. He cites his own costs. It lasts 45 minutes. You end up at +9% because you managed to "hold firm".

You just negotiated one opinion against another opinion. And your company just lost money you didn't have to lose.— The reality of 80% of procurement negotiations

Cost Breakdown and Should-Cost have only one objective: replace your opinions with facts. Put a precise number on each cost item. And enter negotiations knowing exactly which line is overvalued, and by how much.

This is the tool that concretely separates the junior buyer from the senior category manager. Not the title. Not seniority. The ability to walk into a room and say: "Here's our analysis of your cost structure. Let's go through the details."

01

What is Cost Breakdown?

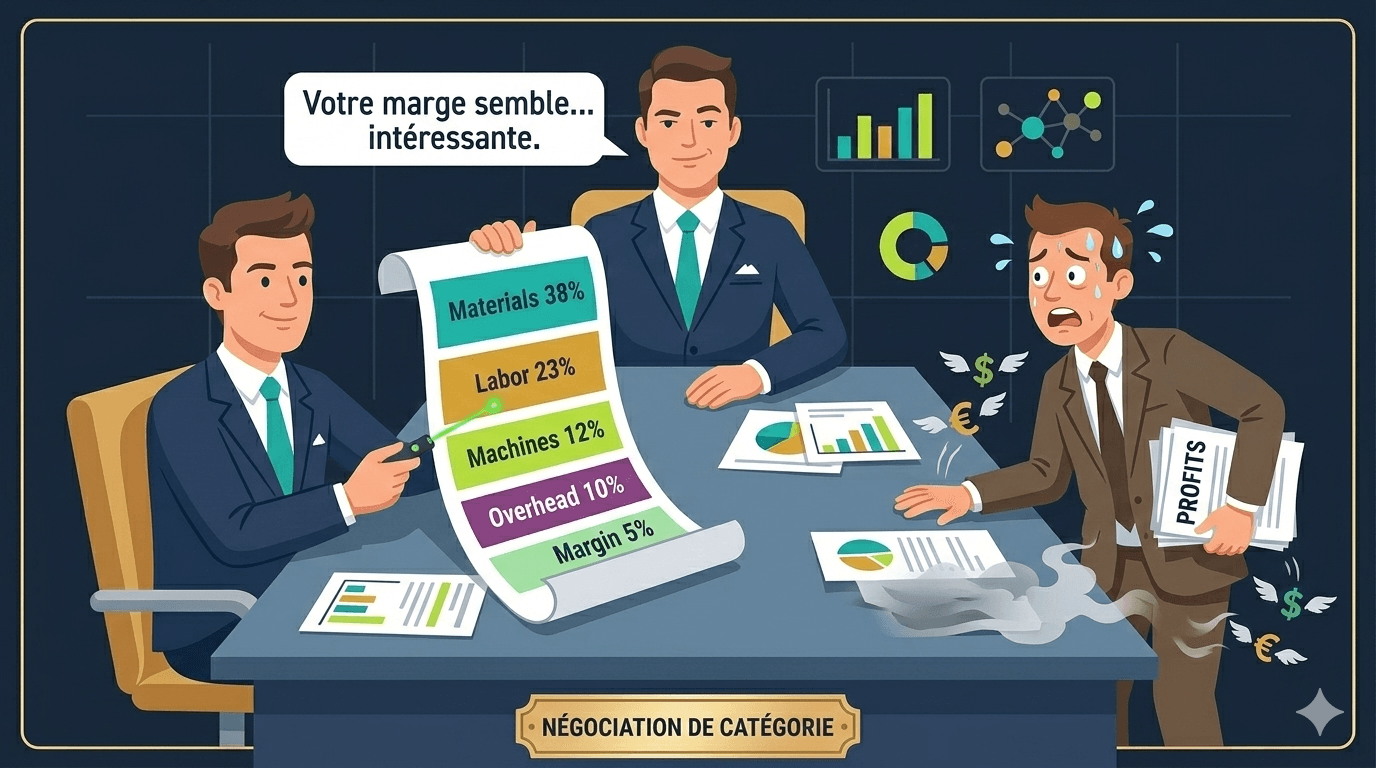

Cost Breakdown is the decomposition of a product or service price into elementary cost items. Instead of an opaque price — "€120 per unit" — you get a complete radiograph of what the supplier actually spends to deliver to you.

For an industrial product, it looks like this:

Example of decomposition — Machined mechanical component

Raw materials

38%

Direct labor

23%

Machine costs / Depreciation

12%

Overhead

10%

Quality / R&D / Certifications

7%

Logistics / Packaging

5%

Supplier margin

5%

Each item has its own cost drivers, its own market benchmarks, and its own negotiation levers. This is the foundation of any serious TCO work.

The 7 standard items

Cost Item | % typical | Main Driver | Negotiation Lever |

|---|---|---|---|

Raw materials | 30–50% | World prices, specifications | Indexation, standardization, substitution |

Direct labor | 15–30% | Hourly rate, productivity, country | Automation, relocation, efficiency |

Machine costs / Depreciation | 8–15% | Investment, utilization rate | Volumes (better utilization rate) |

Overhead | 8–15% | Supplier fixed cost structure | Benchmark, challenge on absorption rate |

Quality / R&D / Certifications | 3–10% | Client requirements, industry standards | Spec rationalization, certif. pooling |

Logistics & Packaging | 2–8% | Distance, transport mode, packaging | Incoterms, returnable packaging, pooling |

Supplier margin | 3–12% | Market, differentiation, relationship | Volume, contract duration, exclusivity |

TOTAL | 100% |

02

Should-Cost : the next level

Cost Breakdown analyzes the actual price the supplier bills you. Should-Cost goes further: it's the reconstruction of the theoretical cost of that same product or service, based on your own market data.

The difference between the two is your most powerful negotiation lever:

If your should-cost on a component is €95 and the supplier is at €120, you don't enter negotiations saying "it's expensive". You enter saying: "Here's our cost model. The gap is €25. We need to understand each item."

03

The 3 levels of maturity

Not all buyers use these tools the same way. There are three distinct levels — and moving from level 1 to level 3 changes everything.

Level 1

The junior buyer

Relies on price comparisons and global benchmarks. Good foundation, but fragile in negotiation if the supplier has technical arguments.

"Your competitor is offering us 20% less for equivalent service."

Level 2

The experienced buyer

Breaks down the 7 items and identifies gaps line by line. Can challenge the supplier item by item with market data.

"Your direct labor rate is €48/h. For this type of production, the market is €36–40/h. What's your justification?"

Level 3

The Expert Category Manager

Reconstructs a complete bottom-up should-cost. Arrives at negotiations with their own cost model, validated by third-party data.

"Our model: materials €42 + direct labor €28 + machines €11 + overhead €9 + logistics €5 = should-cost €95. Your offer: €120. Gap of €25. Let's detail it together."

04

Method for products

For production purchases (components, sub-assemblies, processed materials), cost breakdown is done item by item according to the 7 categories defined above. Here's how to build your analysis in practice.

1

Disassemble the product (physically or by spec)

List each raw material, each machining operation, each transformation step. If you can't do it alone, do it with your engineering team or a specialized consultant. Reverse engineering can also be done visually on physical products.

2

Price each component at market rates

Raw materials: use LME (London Metal Exchange) indices for metals, ICIS for polymers, USDA for agricultural commodities. These are public and free data.

3

Estimate transformation costs

For labor: use Eurostat data or industry salary grids by country. For machines: standard hourly rates by machine type are available in industry publications (CNC machining: €60–150/h depending on complexity and country).

4

Apply overhead and margin

Typical overhead ranges from 20 to 40% of transformation costs. Gross margin in the manufacturing sector typically runs 5–15% depending on specialization level. These ratios are available in industry reports (Xerfi, Dun&Bradstreet, listed company annual reports).

5

Compare and identify gaps

Your should-cost against supplier price. Each positive gap (supplier more expensive) is a question to ask. Each negative gap (supplier cheaper than your model) deserves to be understood — it might be genuine efficiency, or reduced quality.

05

Method for services

Services (IT, consulting, call center, transport, cleaning, maintenance…) break down differently. There are no raw materials, but there are human equivalents that represent 60–80% of total cost.

The typical breakdown of a service

Item | Description | % typical services |

|---|---|---|

Labor (FTE) | Cost of people assigned to your account | 55–70% |

Management / Supervision | Supervisors, project managers, account managers | 8–15% |

Tools / Technology / Licenses | Software, equipment, infrastructure | 5–12% |

Overhead & Real estate | Offices, HR, finance, support | 8–15% |

Training & Recruitment | Onboarding, ongoing training, turnover | 2–5% |

Supplier margin | Target operating profit | 5–15% |

Concrete example: outsourced call center

This is the most pedagogical example because everything can be calculated. Let's say a contract with 50 full-time agents, billed at €32/h per agent.

🔎 Deconstruction

What you pay: €32/h × 50 agents × 1,750h/year = €2.8M/year

What we can reconstruct:

- Agent salary (low-cost country type Morocco): ~€5/h (€12/h all-in)

- Actual occupancy rate: 75–80% → €12 / 0.77 = €15.6 effective agent cost

- Management (1 supervisor per 12 agents ratio): +€2.4/h

- CRM tools + telephony: +€1.2/h

- Overhead (20%): +€3.8/h

- Margin (10%): +€2.3/h

- Reconstructed should-cost: ~€25.3/h

Gap with billed price: €6.7/h × 50 agents × 1,750h = €586,000/year to question in negotiation.

Does this mean the supplier is "stealing" €586k from you? Not necessarily. They might have higher training costs, higher quality agents, better tools. But it's now your question to ask them — not theirs to impose on you.

06

Where to find the data

Should-Cost is only useful if the data you use is reliable. Here are the best sources, organized by cost type.

🏭

Raw materials

- London Metal Exchange (LME)

- ICIS — polymers & chemicals

- Fastmarkets

- USDA — agribusiness

- Platts — energy & petrochemistry

👷

Labor

- Eurostat — salaries by country/sector

- OECD Labour Stats

- Mercer / Towers Watson

- Hays / Robert Half (benchmark)

- Published collective agreements

⚙️

Machine costs

- Industry publications (FIM, UIMM)

- Deloitte / PwC industrial reports

- Trade guilds & associations

- Ask directly (open-book)

- Reverse engineering / competitive quotes

📊

Margins & overhead

- Annual reports of listed competitors

- Xerfi / IBISWorld (sector reports)

- Dun & Bradstreet

- Altares / Infogreffe

- Supplier financial statement analysis

07

In negotiation : two approaches, two contexts

Cost Breakdown and Should-Cost are used differently depending on your Kraljic positioning (you read article #3, right?). Two main contexts:

Strategic Category

Collaborative approach

The supplier is critical, hard to replace. The goal is not to crush them — it's to optimize together. We share cost structures both ways.

"Here are our constraints on the client side. Here's our cost model. What can we do together to find 10% optimization without compromising quality?"

Leverage Category

Competitive approach

The market is competitive, you have alternatives. Cost Breakdown becomes a direct challenge weapon. You've done your homework, you ask the questions that matter.

"Our analysis shows your direct labor costs appear superior to market by 25%. You have until Friday to explain why, or revise your offer."

The distinction is important. Using the competitive approach on a strategic, irreplaceable supplier risks destroying a relationship you need. Using the collaborative approach on a category where you have 12 alternatives leaves money on the table.

08

Classic mistakes (and how to avoid them)

09

Cost Breakdown's place in your complete toolkit

If you've followed the series from the start, you now have a complete analytical toolkit. Here's how all the tools feed each other:

🔗 The logical sequence

Spend Analysis → identifies priority categories and total spend

Porter's Five Forces → evaluates your negotiating position on these categories

Kraljic Matrix → prioritizes where to deploy aggressive vs collaborative strategy

Supplier Segmentation → determines which suppliers to go in-depth with

Cost Breakdown / Should-Cost ← You are here → provides factual arguments for negotiation

Category Strategy Canvas → synthesizes all of this into a 2–3 year action plan

Cost Breakdown without Kraljic is analyzing the wrong categories. Should-Cost without Porter is not knowing if you have the leverage to use your arguments. And both without the Strategy Canvas is executing without a plan.

The tool has value only in sequence. This is what makes the difference between isolated analysis and true category strategy.

Negotiation is not when you're looking for your arguments. It's when you're using them — because you built them three weeks ago.— Basic principle of Category Management

In summary

Cost Breakdown and Should-Cost transform negotiation from a vague power dynamic into a factual, structured exchange. They allow you to move from "I think it's too expensive" to "here's why it's too expensive, line by line".

- The Cost Breakdown decomposes the current price into elementary items

- The Should-Cost reconstructs the theoretical cost from market data

- The gap between the two is your quantified negotiation basis

- The approach (collaborative vs competitive) depends on your Kraljic position

- The data is accessible — the key is looking for it

Next time a supplier announces a price increase, you won't have to negotiate an opinion. You'll have your model. And it will be the one dictating the conversation.

Next article in the series

Article #6 : Category Strategy Canvas — How to synthesize the 5 tools in 1 page and align your stakeholders around a clear action plan.

Liked this? The monthly newsletter goes deeper: one map, every first Tuesday.

The monthly map, every first Tuesday at 07:30. One-click unsubscribe.

First Tuesday of every month, 07:30 CET. One-click unsubscribe.

In this series

Category Strategy Canvas : Transform 5 weeks of analysis into 1 page that convinces your CEO

Five weeks of category analysis condensed into one page that convinces a CEO. The canvas, the 9 blocks, and the boardroom-ready format that closes loops.

10 March 2026Next → · Procurement MasteryKraljic Matrix : Stop treating all your categories the same way

Managing semiconductors like office supplies wastes time and savings. The Kraljic matrix tells you where to prioritise — and where to stop overinvesting.

10 March 2026From the same seriesThe 6 Essential Tools Every Category Manager should Master

The 6 tools every category manager must master — and the exact order to use them. The complete framework: spend analysis through to category strategy canvas.

10 March 2026