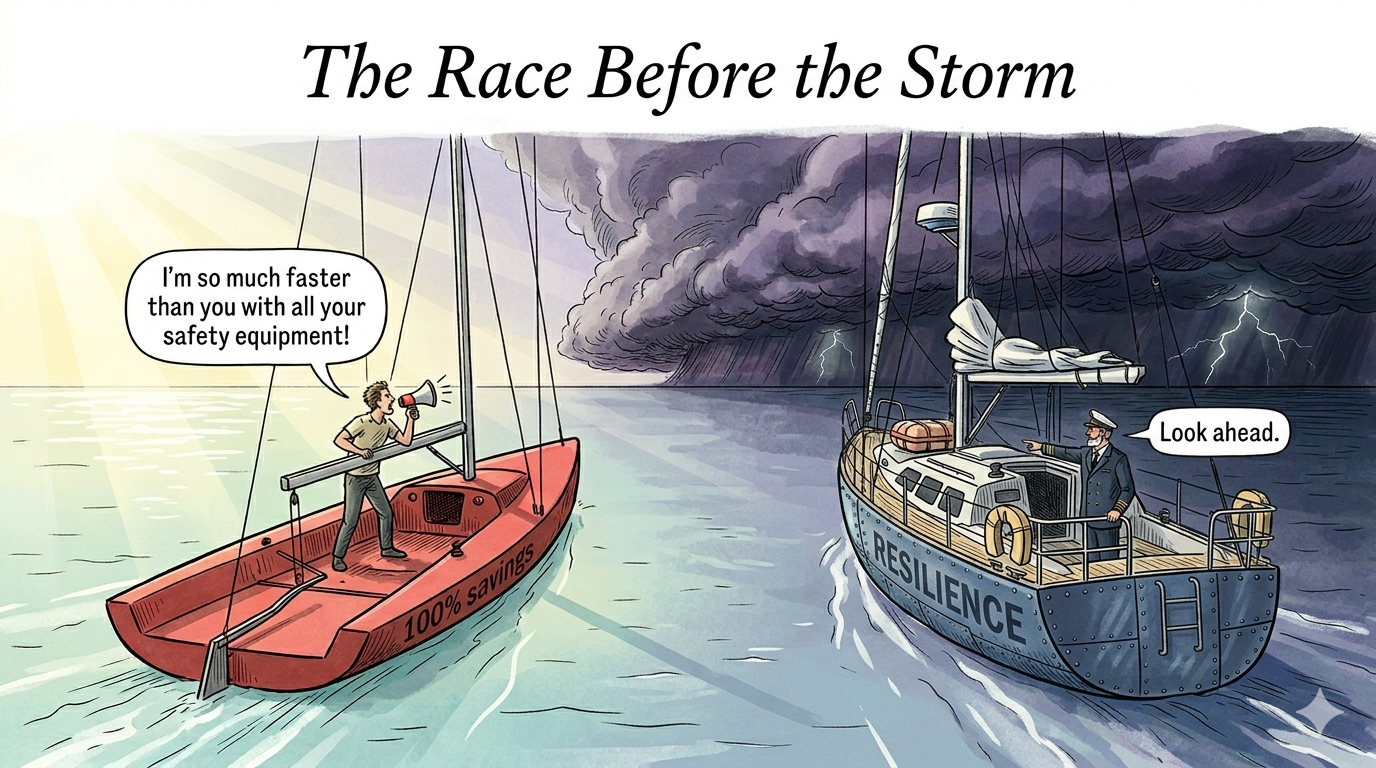

They reward those that invested in resilience.

For the first time in 20 years, savings are no longer the #1 strategic priority for procurement teams.

69% of CPOs now rank risk management and resilient supply chains ahead of cost reduction (Deloitte, Supply Chain Resilience, 2025). For a function that has been measured almost exclusively on the savings line for two decades, that’s a real shift — and it didn’t happen because boards suddenly discovered ESG. It happened because the cost of not investing in resilience finally became visible on the P&L.

2026: the landscape looks nothing like what most CPOs planned for. Tariff wars keep escalating — 82% of supply chain leaders say their operations are directly affected by new trade barriers (McKinsey, Supply Chain Risk Pulse 2025). Input prices are wild — RAM, servers, GPUs and other commodities flaming up, margins under real pressure. The EU’s Corporate Sustainability Due Diligence Directive got pushed to 2029, but the due-diligence requests from large buyers haven’t slowed down a bit.

I’m watching two very different stories unfold.

The two teams

On one side, procurement teams that treated resilience as a strategic investment — years before the current storm hit.

On the other, teams that optimised purely for cost, convinced that disruption was someone else’s problem.

The numbers tell us which camp is winning.

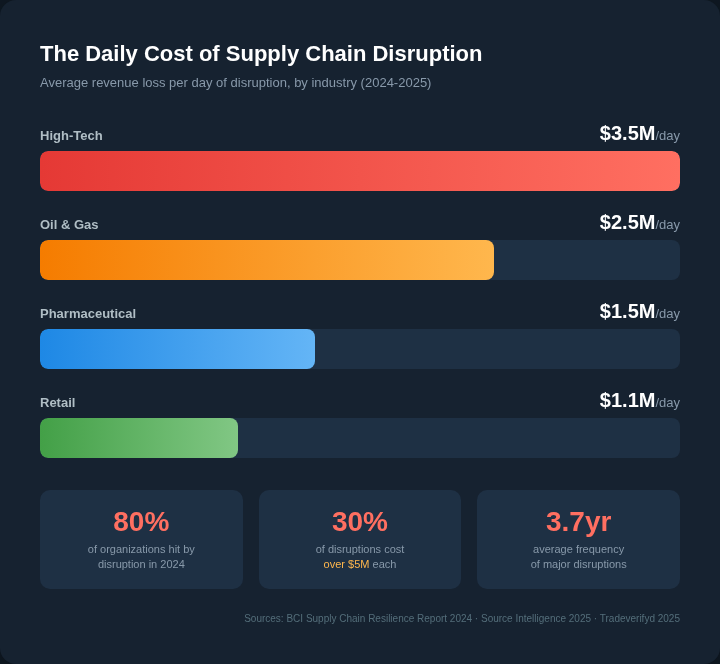

In 2024 alone, 80% of organizations experienced at least one significant supply chain disruption — up from the year before (BCI Supply Chain Resilience Report, 2024). Nearly 30% of those cost more than $5M each, with average daily losses of $1.5M in pharma, $2.5M in oil & gas, $3.5M in high-tech (Source Intelligence, 2025).

And despite all of this, 43% of organisations still have limited or no visibility on the performance of their tier-1 suppliers (Tradeverifyd, 2025). The same finding has been repeated for years now — and the gap is widening between the leaders that have built real-time analytics and AI on top of their supply base, and those still working from a quarterly Excel export.

Resilience is now a P&L line

Boards are waking up. BCG’s 2025 analysis, Balancing Cost and Resilience, puts it without much padding: the (false) choice between cost efficiency and supply chain resilience is over.

McKinsey’s 2025 Supply Chain Risk Pulse survey adds an uncomfortable detail — only a small fraction of executives believe their own board genuinely understands supply chain risk. So when the next disruption hits, the board is caught flat-footed, not because the data wasn’t there but because nobody translated it into board language in time.

The companies getting this right are building what McKinsey calls « structural risk reduction » — resilience embedded in the architecture of the supply chain, not a crisis-response reflex pulled out when things break. Boards are now enforcing four new governance rules: quantified business cases for resilience investments, segmented strategies by category criticality, structural risk reduction over reactive response, and resilience treated as an architectural capability (Supply Chain Intelligence, 2026).

The nearshoring dividend

28% of EU companies now plan to nearshore (QIMA, 2025). It’s not a plan anymore, it’s already in motion — inspection demand in Mediterranean hubs surged in Q2 2025: Morocco +53% YoY, Egypt +73%, Tunisia +35%, Turkey +27% (QIMA, 2025).

The interesting bit: the companies driving this shift didn’t start because of tariffs. They started in 2023-2024, before the escalation. They paid a 5 to 15% premium for regional suppliers, and at the time their CFOs questioned the call.

Fast-forward to Q1 2026. With new tariffs on Chinese goods and shipping volatility, those « expensive » regional suppliers are now 10 to 15% cheaper on a total-cost basis than the single-region Asian setups their competitors are scrambling to restructure.

The WTO’s 2025 work confirms the broader pattern: companies operating within free trade agreements cut their tariff costs by 10% — but only if they had already aligned their supply base to take advantage of those agreements (CPSCP, 2025). You can’t restructure a supply chain in 90 days. The ones winning today started years ago.

In parallel, 82% of supply chain organisations increased IT spending in 2025 (Tradeverifyd, 2025) — not out of innovation curiosity, but because boards are demanding visibility, real-time monitoring and data-driven decisions. Capabilities the mature procurement functions built three years ago, and the fragile ones are now buying under pressure.

ESG isn’t virtue. It’s intelligence.

This is probably the most misunderstood part of the conversation.

A rigorous ESG assessment of your supply base forces you to look at supplier financial health, operational risk, social stability and strategic direction — that’s intelligence no RFP, and no negotiation, will ever surface.

NYU Stern’s meta-analysis of more than 1,000 studies found 58% showed a positive link between ESG performance and financial returns, against only 8% showing a negative one (NYU Stern / Seneca ESG, 2023). MSCI’s 2024 data went further: companies in the top ESG quintile outperformed those in the bottom quintile over 2012–2023 (Seneca ESG, 2025).

The number that should make every CPO sit up: supply chain emissions average 26 times a company’s direct operational emissions (EcoVadis, 2026). 70% of the carbon footprint sits in Scope 3 — and yet only 15% of CDP-disclosing companies have set Scope 3 targets (EcoVadis, 2026). That gap is both a regulatory landmine and, for the teams that close it early, a serious competitive edge.

The EU Omnibus revisions pushed CSDDD compliance to 2029 and narrowed the scope to companies with more than 5,000 employees and €1.5B+ turnover (EcoVadis, 2026). But the in-scope groups are already cascading their due-diligence requirements down to their suppliers — today. If you supply a CAC 40 company, you’ll be asked for ESG data whether the directive applies to you directly or not.

What to do this week

If you’re a CPO or procurement leader wondering where to start, three moves that take days, not months:

- Map your concentration risk. Top 20 suppliers by spend: how many alternative sources exist? How long to switch? What’s the revenue impact of a 30-day outage? If you can’t answer in under an hour, the visibility gap is your first project.

- Calculate your cost of fragility. Add up last year’s disruption costs: emergency sourcing premium + expedited shipping + production downtime + customer penalties + internal hours spent firefighting. That total is your « cost of not investing in resilience ». Put it in front of your CFO.

- Start one ESG pilot. Pick your most critical category, run the top 5 suppliers through basic ESG criteria. You’ll learn more about your supply chain in that exercise than in a year of QBRs.

The best time to invest in supply chain resilience was 2022. The second best time is today — keeping in mind that « today » will probably only show measurable results in 12 to 18 months. Which is exactly the question for the GMs and CFOs reading this: can you afford to wait another year?

Want to talk about how we can future-proof your procurement together? Drop me a message.