In April 2021, the European Parliament introduced a new regulation called Corporate Sustainability Reporting Directive. This directive will require most of the biggest 50,000 companies in Europe to analyze and disclose their sustainability impact as part of their annual disclosure, starting from January 2025 and covering the fiscal year 2024. In addition to the extended scope of the CSRD, which goes beyond just carbon footprint calculation and includes social and ethics, maybe the biggest change is that this reporting now needs to be done in a standardized and comparable way across Europe meaning that companies now operate under the same set of hypothesis when it comes to developing their sustainability plan. This represents an important step toward making businesses understand their impact, but also in making sure their claims in terms of sustainability are better monitored.

Who is concerned by the CSRD obligation?

Reporting requirement: the EU’s ambition

The Corporate Sustainability Reporting Directive (CSRD) ambition is to cover the largest part of the businesses in Europe, and its scope is going to increase over time, until 2028 when it will apply to any companies satisfying quite low criteria: being a listed company in EU, or being an EU non-listed company with over 40M€ in turnover, any outside company that hires more than 500 people or 150M€ in turnover. There are finer details for each of these rules, but they do represent a big change as today, companies with 40M€ turnover have close to no obligations in regards to sustainability, and the scale of the obligation will require profound changes and a lot of education.

Large listed undertakings

These include any companies listed on an EU-regulated market exchange—except for ‘micro undertakings’ that fail to meet two of the following three criteria on consecutive balance sheet dates:

- at least EUR 350,000 (450,000$) in total assets.

- at least EUR 700,000 (850,000$) in net turnover (revenue).

- at least 10 employees (average) throughout the year.

EU-based large undertakings, listed or not

These include any listed or non-listed companies that meet two of the following three criteria on any two consecutive balance sheet dates:

- at least EUR 20 (25$) million in total assets.

- at least EUR 40 (50$) million in net turnover.

- at least 250 employees (average) during the year.

‘Third-country’ undertakings

These include non EU parent companies of EU subsidiaries, with annual EU revenues of at least EUR 150 million in the most recent two years, and also own:

- a large EU-based undertaking, or

- an EU-based subsidiary with securities listed on an EU-regulated market exchange, or

- an EU branch office with at least EUR 40 million in net turnover.

Thus, the CSRD casts a wide net to ensure that a significant number of companies, across different sectors and sizes, are making sustainability central to their business practices.

The phasing of the CSRD reporting obligation

A modest start for 2025

While the EU’s ambition is to cover the majority of businesses by 2028, the approach is going to be progressive and only the largest companies will have to report on CSRD in the first year. Indeed, only companies that already have to comply with NFRD (Non-Financial Reporting Disclosure) will have to start reporting on CSRD, meaning that this is “only” a change in improved methodology and format for these companies. This represents about 11,000 companies and leaves a substantial segment of the market without the same level of scrutiny and accountability when it comes to sustainability.

The EU plan to extend the CSRD reporting obligation

The phasing of the CSRD obligation will be made progressively until 2028 when the full criteria listed above will be enforced. By 2026, the criteria are already so much lowered that it starts to be really significant, though again it only applies to listed companies! Overall, it should cover about 50,000 companies, which is only 0,2% of the 23M businesses in Europe that will have to report on CSRD. The obligation is leaving the vast majority of smaller businesses outside of its scope, surely, in an attempt to not make business impossible (or at least too difficult) to start.

While there is no clear figure of how much the EU GDP this will cover, it should be a substantial proportion, as taking the example of France, only the CAC40 (top 40 French companies) represents already 51% of the French GDP. While conscious that this % cannot be used for all EU, it can give a positive outlook.

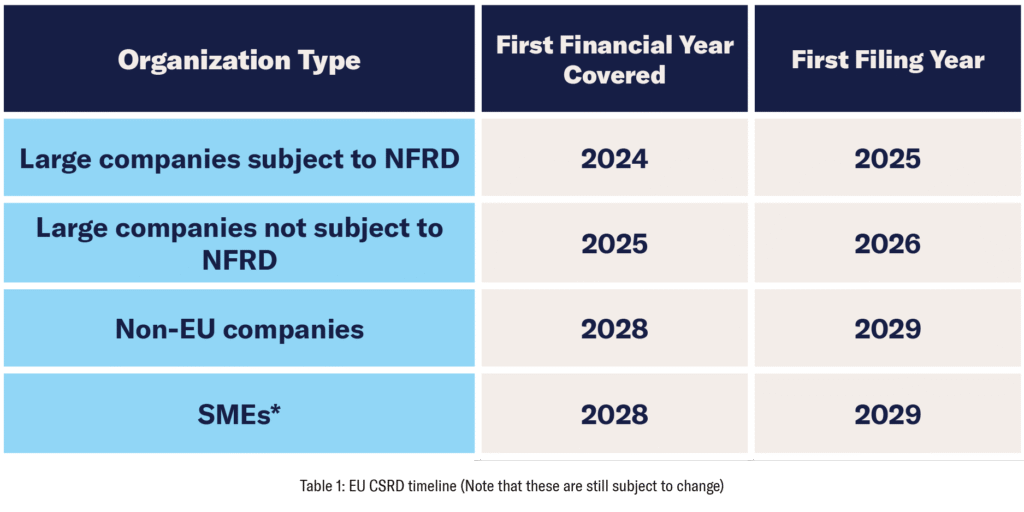

Starting in financial year 2024 (and reporting in 2025): Compliance is mandated for organizations (or ‘entities’) already mandated to comply with the NFRD. This includes all organizations listed in an EU-regulated market with 500 or more employees.

Starting in financial year 2025 (reporting in 2026): Compliance is mandated for large listed undertakings (see above) not already mandated to comply with the NFRD.

Starting in financial year 2026 (reporting in 2027): Compliance is mandated for small and medium-sized undertakings (also called small and medium-sized entities, or SMEs)—companies listed on an EU-regulated market that meet at least two or three of the following criteria:

- at least EUR 4 (5*) million in total assets.

- at least EUR 8 (10*) million in net turnover.

- at least 50 employees average throughout the year.

Starting in the financial year 2028 (reporting 2029): Compliance is mandated for third-country undertakings.

Corporate Sustainability reporting expectations :

Deliverables

The main deliverable is a comprehensive annual sustainability report. This report should detail the company’s environmental and social impacts, sustainability policies, goals, and the progress made towards achieving these goals. The report should also include proposals for mitigating any significant negative impacts and align with the obligation to reach carbon neutrality by 2050.

The Corporate Sustainability Reporting Directive (CSRD) covers a wide array of sustainability impacts, going beyond just carbon emissions. Companies will need to provide information on their environmental, social, employee matters, respect for human rights, anti-corruption and bribery issues. This includes, but is not limited to, greenhouse gas emissions, water and energy use, and the impact on biodiversity. The CSRD aims to provide a comprehensive view of a company’s sustainability performance and assess its double-materiality (an important concept that recognizes the impact materiality of sustainability topics at the same level as the financial ones that have been the core of annual reports for decades now).

This report needs to be clear, concise, and accessible to stakeholders and must adhere to the standardized reporting format to ensure comparability across different companies and sectors. This will allow the public, investors, and other stakeholders to assess and compare the sustainability performance of different companies.

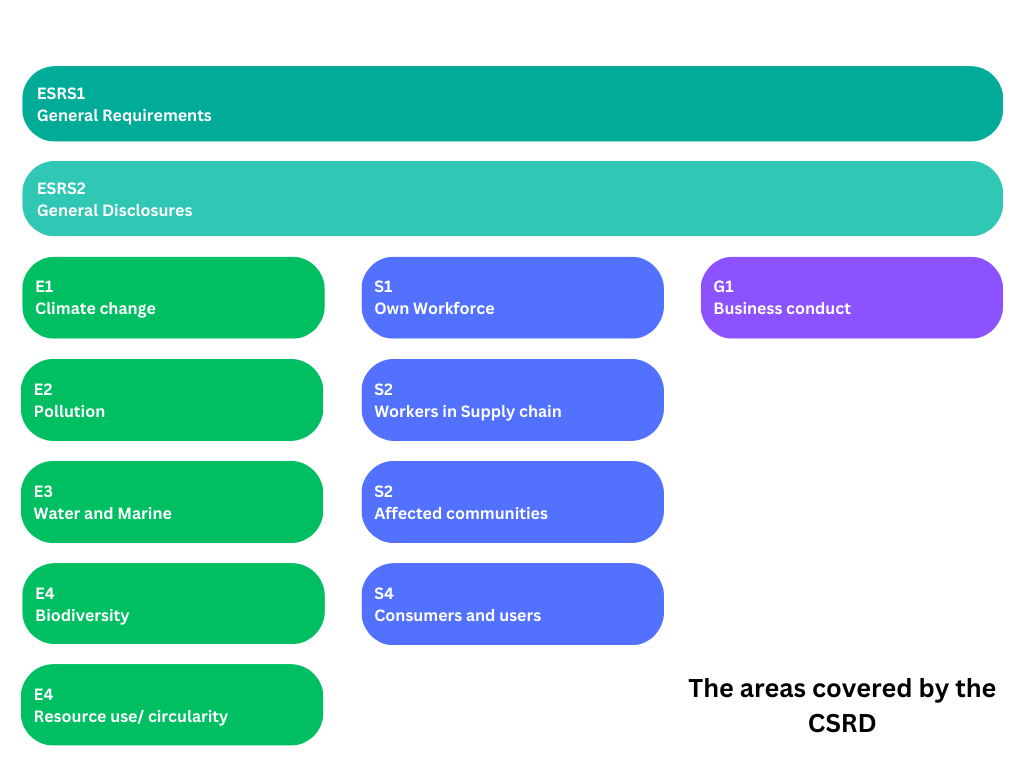

The European Commission is expected to deliver the first draft of the template for Corporate Sustainability Reporting (CSR) submissions by the end of 2022, but as far as I know, this was not yet done. The proposed approach is to base the reporting on 12 European Sustainability Reporting Standards (ESRS) , which detail disclosures and metrics across sustainability matters in four (4) categories:

- Cross-cutting: General principles and general disclosures.

- Environmental: Climate change, pollution, water and marine resources, biodiversity and ecosystems, resource use, and circular economy.

- Social: Own workforce, workers in the value chain, affected communities, consumers and end-users.

- Governance: Business conduct.

Cross-cutting reporting is required of all organizations governed by the CSRD, while environmental, social and governance reporting is mandatory for those organizations that consider them material.

Penalties for Non-Compliance

Failure to comply with the Corporate Sustainability Reporting Directive (CSRD) can result in significant penalties. While the exact penalties can vary by country, they may include financial fines, reputational damage, and increased scrutiny from regulators.

In addition to financial penalties, companies that fail to comply may also face legal consequences. These can range from lawsuits by shareholders, who may argue that the company’s lack of transparency constitutes a breach of fiduciary duty, to regulatory actions by government agencies.

Furthermore, non-compliance can lead to reputational damage. In an era where consumers and investors are becoming increasingly conscious of the environmental and social impacts of businesses, companies that fail to disclose their sustainability impact may find themselves at a competitive disadvantage.

Summary and Conclusion

Pros

- The Corporate Sustainability Reporting Directive (CSRD) promotes transparency among large companies in Europe.

- It could lead to more sustainable business practices as companies analyze and disclose their environmental impact.

- The directive will provide a standardized way of reporting across Europe, making comparisons and analyses easier.

- It could stimulate competition among companies to be more sustainable.

- The CSRD could potentially increase trust among consumers and stakeholders due to increased transparency.

Cons

- Compliance with the CSRD could impose additional administrative and financial burdens on companies.

- Smaller companies or those just outside the top 50,000 may not be subjected to the same scrutiny, potentially creating an uneven playing field.

- The standardized reporting may not accurately reflect the unique sustainability challenges and efforts of each company.

- The effectiveness of the CSRD in promoting real change versus just “greenwashing” or superficial sustainability efforts is not guaranteed.

- Companies may face reputational risks if their sustainability reports reveal negative impacts.

In conclusion, the introduction of the Corporate Sustainability Reporting Directive (CSRD) by the European Parliament is indeed a significant first step towards making sustainability central to business practices. While it does impose new responsibilities and obligations on companies, it also provides an opportunity for businesses to become leaders in sustainability. Yes, the effort required for compliance is substantial. Companies will need to assess their environmental and social impacts, develop comprehensive sustainability policies, and consistently monitor their progress. However, this effort is not without its rewards. By driving transparency and encouraging sustainable practices, the CSRD promotes a level playing field where companies are rewarded for their commitment to sustainability. It’s a challenging yet crucial path forward, and the benefits far outweigh the costs. In the long run, businesses, stakeholders, and the environment stand to gain from this directive.

We will cover each component of the reporting in more detail so stay tuned for more information on the topic!