Cost Breakdown & Should-Cost : Negotiate with facts (not opinions)

The difference between a buyer who suffers price increases and a category manager who contests them — this is that tool.

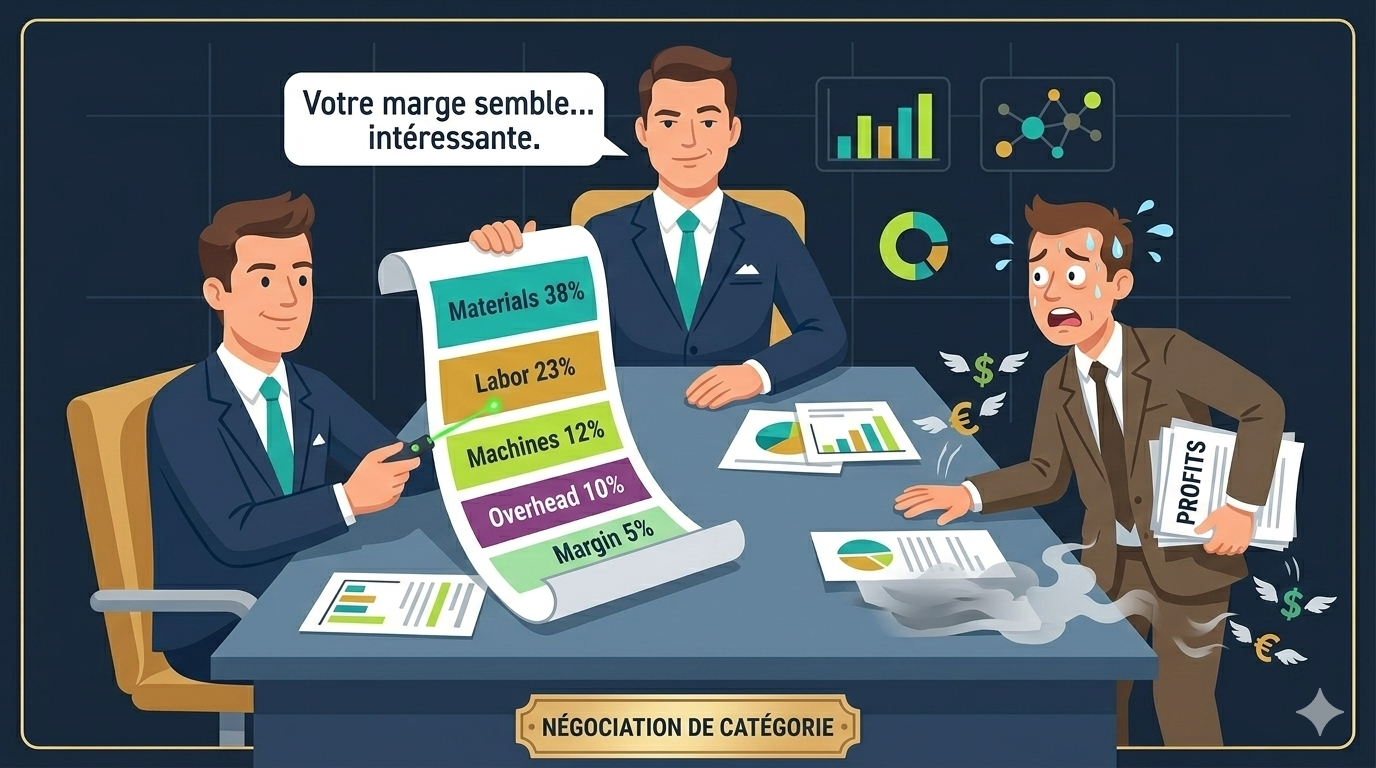

A lived, universal scene. You’re in a negotiation. The supplier puts their cards on the table: +14% increase on the next contract. You say it’s too much. He says it’s inevitable. You cite inflation. He cites his own costs. It lasts 45 minutes. You end up at +9% because you managed to “hold firm”.

You just negotiated one opinion against another opinion. And your company just lost money you didn’t have to lose.— The reality of 80% of procurement negotiations

Cost Breakdown and Should-Cost have only one objective: replace your opinions with facts. Put a precise number on each cost item. And enter negotiations knowing exactly which line is overvalued, and by how much.

This is the tool that concretely separates the junior buyer from the senior category manager. Not the title. Not seniority. The ability to walk into a room and say: “Here’s our analysis of your cost structure. Let’s go through the details.”

What is Cost Breakdown?

Cost Breakdown is the decomposition of a product or service price into elementary cost items. Instead of an opaque price — “€120 per unit” — you get a complete radiograph of what the supplier actually spends to deliver to you.

For an industrial product, it looks like this:

Each item has its own cost drivers, its own market benchmarks, and its own negotiation levers. This is the foundation of any serious TCO work.

The 7 standard items

| Cost Item | % typical | Main Driver | Negotiation Lever |

|---|---|---|---|

| Raw materials | 30–50% | World prices, specifications | Indexation, standardization, substitution |

| Direct labor | 15–30% | Hourly rate, productivity, country | Automation, relocation, efficiency |

| Machine costs / Depreciation | 8–15% | Investment, utilization rate | Volumes (better utilization rate) |

| Overhead | 8–15% | Supplier fixed cost structure | Benchmark, challenge on absorption rate |

| Quality / R&D / Certifications | 3–10% | Client requirements, industry standards | Spec rationalization, certif. pooling |

| Logistics & Packaging | 2–8% | Distance, transport mode, packaging | Incoterms, returnable packaging, pooling |

| Supplier margin | 3–12% | Market, differentiation, relationship | Volume, contract duration, exclusivity |

| TOTAL | 100% |

Should-Cost : the next level

Cost Breakdown analyzes the actual price the supplier bills you. Should-Cost goes further: it’s the reconstruction of the theoretical cost of that same product or service, based on your own market data.

The difference between the two is your most powerful negotiation lever:

The 3 levels of maturity

Not all buyers use these tools the same way. There are three distinct levels — and moving from level 1 to level 3 changes everything.

The junior buyer

The experienced buyer

The Expert Category Manager

Method for products

For production purchases (components, sub-assemblies, processed materials), cost breakdown is done item by item according to the 7 categories defined above. Here’s how to build your analysis in practice.

Disassemble the product (physically or by spec)

Price each component at market rates

Estimate transformation costs

Apply overhead and margin

Compare and identify gaps

Method for services

Services (IT, consulting, call center, transport, cleaning, maintenance…) break down differently. There are no raw materials, but there are human equivalents that represent 60–80% of total cost.

The typical breakdown of a service

| Item | Description | % typical services |

|---|---|---|

| Labor (FTE) | Cost of people assigned to your account | 55–70% |

| Management / Supervision | Supervisors, project managers, account managers | 8–15% |

| Tools / Technology / Licenses | Software, equipment, infrastructure | 5–12% |

| Overhead & Real estate | Offices, HR, finance, support | 8–15% |

| Training & Recruitment | Onboarding, ongoing training, turnover | 2–5% |

| Supplier margin | Target operating profit | 5–15% |

Concrete example: outsourced call center

This is the most pedagogical example because everything can be calculated. Let’s say a contract with 50 full-time agents, billed at €32/h per agent.

- Agent salary (low-cost country type Morocco): ~€5/h (€12/h all-in)

- Actual occupancy rate: 75–80% → €12 / 0.77 = €15.6 effective agent cost

- Management (1 supervisor per 12 agents ratio): +€2.4/h

- CRM tools + telephony: +€1.2/h

- Overhead (20%): +€3.8/h

- Margin (10%): +€2.3/h

- Reconstructed should-cost: ~€25.3/h

Does this mean the supplier is “stealing” €586k from you? Not necessarily. They might have higher training costs, higher quality agents, better tools. But it’s now your question to ask them — not theirs to impose on you.

Where to find the data

Should-Cost is only useful if the data you use is reliable. Here are the best sources, organized by cost type.

Raw materials

- London Metal Exchange (LME)

- ICIS — polymers & chemicals

- Fastmarkets

- USDA — agribusiness

- Platts — energy & petrochemistry

Labor

- Eurostat — salaries by country/sector

- OECD Labour Stats

- Mercer / Towers Watson

- Hays / Robert Half (benchmark)

- Published collective agreements

Machine costs

- Industry publications (FIM, UIMM)

- Deloitte / PwC industrial reports

- Trade guilds & associations

- Ask directly (open-book)

- Reverse engineering / competitive quotes

Margins & overhead

- Annual reports of listed competitors

- Xerfi / IBISWorld (sector reports)

- Dun & Bradstreet

- Altares / Infogreffe

- Supplier financial statement analysis

In negotiation : two approaches, two contexts

Cost Breakdown and Should-Cost are used differently depending on your Kraljic positioning (you read article #3, right?). Two main contexts:

Collaborative approach

Competitive approach

The distinction is important. Using the competitive approach on a strategic, irreplaceable supplier risks destroying a relationship you need. Using the collaborative approach on a category where you have 12 alternatives leaves money on the table.

Classic mistakes (and how to avoid them)

Using a should-cost that’s too theoretical

Ignoring differentiated quality

Not updating the model

Using should-cost to attack without relationship

Confusing targeted savings with should-cost gap

Cost Breakdown’s place in your complete toolkit

If you’ve followed the series from the start, you now have a complete analytical toolkit. Here’s how all the tools feed each other:

Cost Breakdown without Kraljic is analyzing the wrong categories. Should-Cost without Porter is not knowing if you have the leverage to use your arguments. And both without the Strategy Canvas is executing without a plan.

The tool has value only in sequence. This is what makes the difference between isolated analysis and true category strategy.

Negotiation is not when you’re looking for your arguments. It’s when you’re using them — because you built them three weeks ago.— Basic principle of Category Management

In summary

Cost Breakdown and Should-Cost transform negotiation from a vague power dynamic into a factual, structured exchange. They allow you to move from “I think it’s too expensive” to “here’s why it’s too expensive, line by line”.

- The Cost Breakdown decomposes the current price into elementary items

- The Should-Cost reconstructs the theoretical cost from market data

- The gap between the two is your quantified negotiation basis

- The approach (collaborative vs competitive) depends on your Kraljic position

- The data is accessible — the key is looking for it

Next time a supplier announces a price increase, you won’t have to negotiate an opinion. You’ll have your model. And it will be the one dictating the conversation.

Next article in the series

- Article #0 — Introduction · Roadmap

- Article #1 — Spend Analysis : Where does the money go?

- Article #2 — Porter’s Five Forces : What’s your market position?

- Article #3 — Kraljic Matrix : Where should you prioritize?

- Article #4 — Supplier Segmentation : How to manage your portfolio?

- Article #5 — Cost Breakdown & Should-Cost : How to negotiate with facts? ← You are here

- Article #6 — Category Strategy Canvas : What’s your action plan?