After the EU announced its ambitious €1 trillion investment as part of the European Green Deal, the challenge was determining which activities would drive the most sustainable outcomes. How to define where the money should go ?

That’s when and why the Eu taxonomy came about. It may not be the most thrilling document to read, but it is a cornerstone in defining what counts as a truly sustainable economic activity. Its importance lies in offering clarity on where funds should go to effectively support the green transition. The Taxonomy provides a structured framework for this, ensuring that the enormous funding aligns with activities that genuinely contribute to climate and environmental goals, preventing greenwashing and encouraging responsible investments.

The Eu taxonomy is one of the foundations of the EU approach to sustainability, and understanding the principles it lays out is key to u understand every subsequent regulations : CSRD, ESPR, EU green bonds etc…

So in this article, I explain what makes, for the EU, a sustainable activity, and then look at some of the impacts it has had to date.

Link to EU text here.

1. What is the EU Taxonomy?

Dates and Context

The EU Taxonomy Regulation, introduced in July 2020, is part of the EU’s broader strategy to achieve climate neutrality by 2050 and meet the objectives of the European Green Deal. It is designed to steer investments towards projects that align with the EU’s sustainability goals, making it a key instrument in addressing climate change and promoting environmental resilience.

Objective

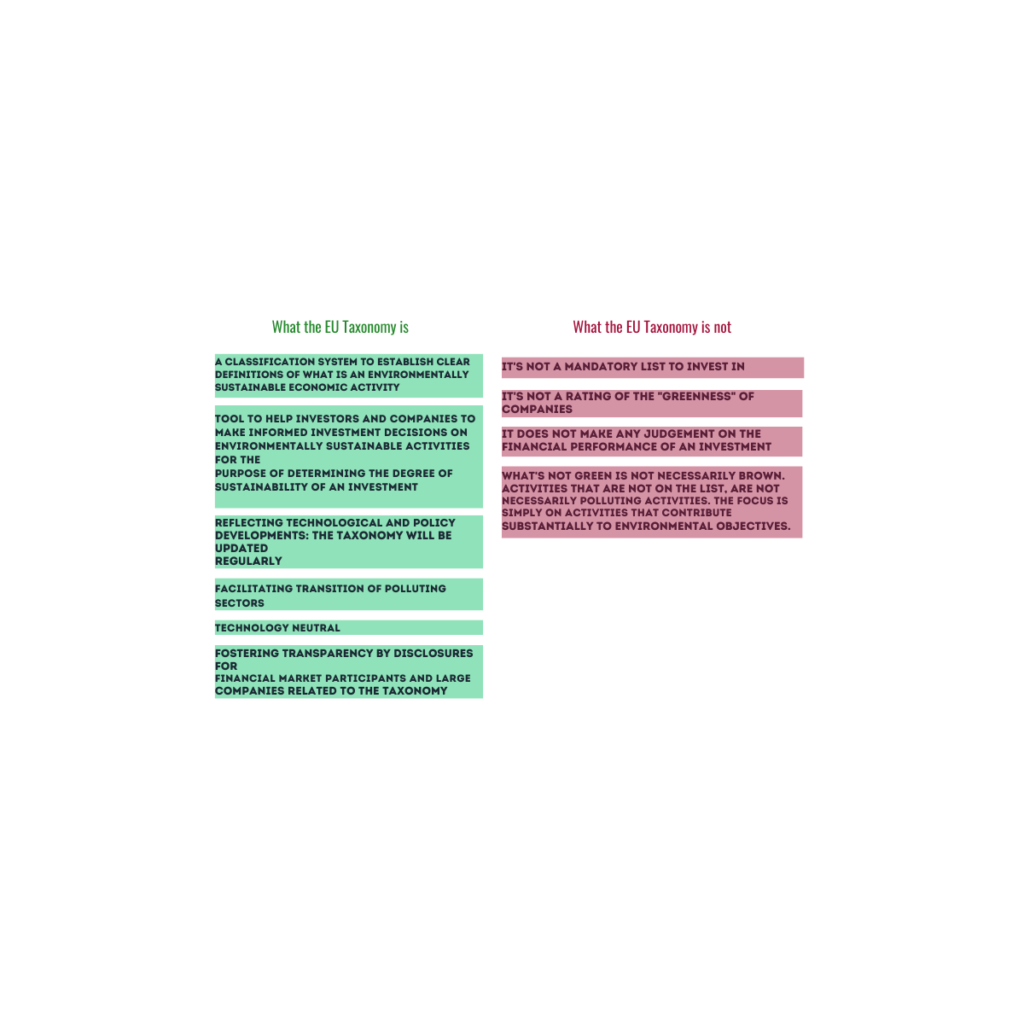

The EU Taxonomy’s main objective is to provide a standardized classification system that clearly defines which economic activities can be considered environmentally sustainable. This helps investors, companies, and policymakers support projects that contribute significantly to environmental objectives, thus ensuring that capital flows toward the activities most critical for achieving a sustainable future.

The Four Overarching Principles

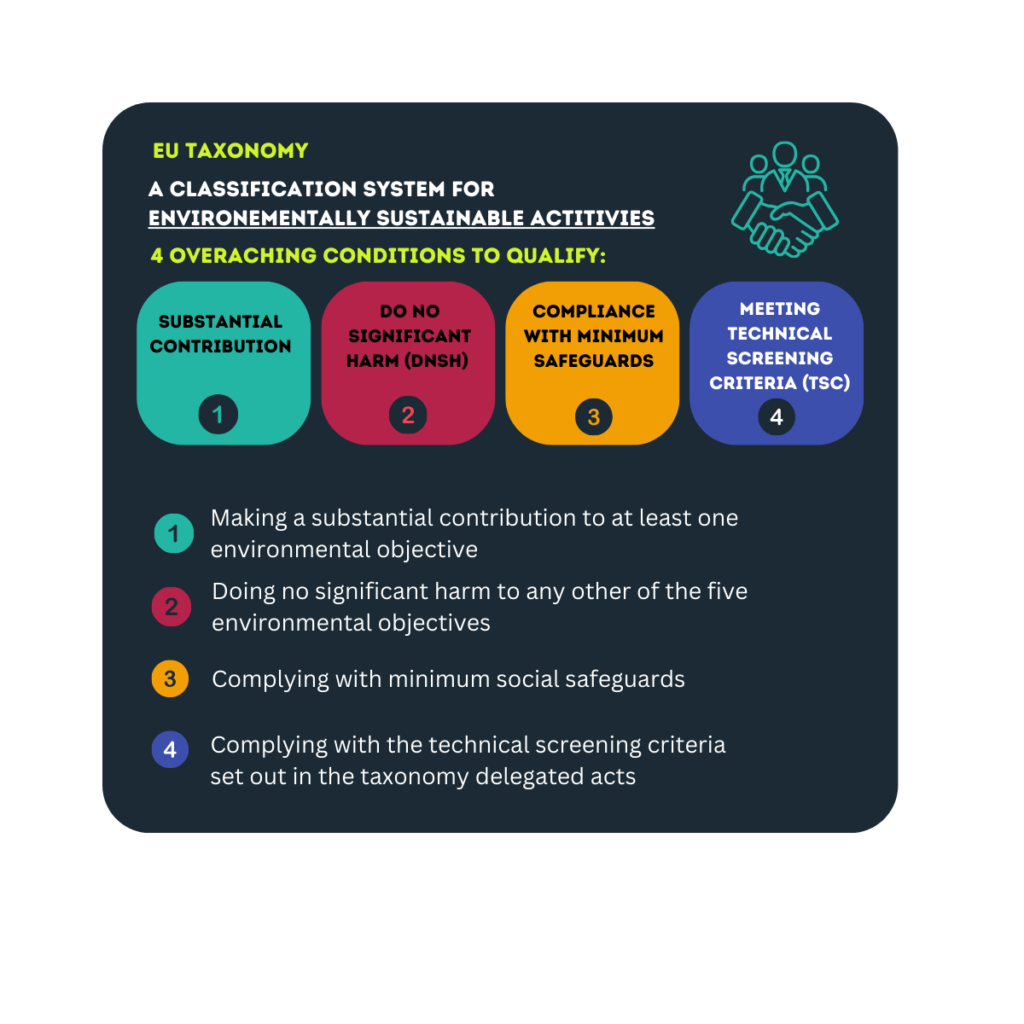

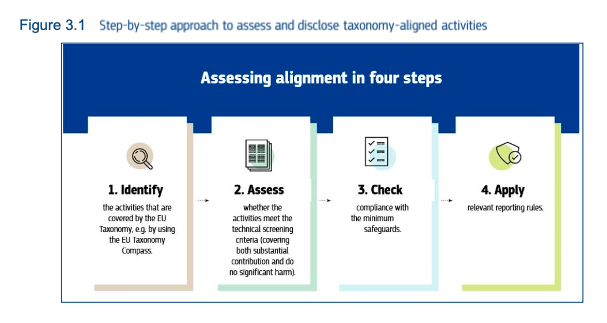

To qualify as environmentally sustainable under the EU Taxonomy, an economic activity must meet four overarching principles:

- Substantial Contribution to at least one Environmental Objectives

- The activity must contribute substantially to at least one of the six environmental objectives. This means that the activity should play a significant role in advancing a specific sustainability goal, such as reducing emissions or promoting the circular economy. For example, a company installing energy-efficient technology in manufacturing can substantially contribute to climate change mitigation.

- Do No Significant Harm (DNSH) on any of the other five environmental objective

- While contributing to one environmental goal, the activity must not significantly harm any of the other five environmental objectives. This principle ensures that progress in one area (e.g., reducing emissions) does not come at the expense of other areas (e.g., biodiversity or pollution control). For instance, while renewable energy projects may reduce carbon emissions, they could harm biodiversity if not planned responsibly as they require many rare earths.

- Compliance with Minimum Social Safeguards

- The activity must comply with minimum social safeguards, such as adhering to international labor standards, human rights, and governance principles. This ensures that businesses pursuing environmental sustainability also respect human dignity, fair labor practices, and the rule of law, maintaining a balance between social and environmental impacts.

- Meeting Technical Screening Criteria (TSC)

- Finally, the activity must meet the Technical Screening Criteria set by the Commission, which are specific benchmarks for each environmental objective. These criteria define what qualifies as a substantial contribution, ensuring that only the most impactful activities are recognized as sustainable.

In addition to environmentally sustainable activities, the EU Taxonomy also recognizes “transition” and “enabler”activities.

- Transition activities are found in carbon-intensive sectors such as steel, cement, and aviation. These industries are essential for the economy but must transition to greener technologies, reducing their emissions while continuing their operations.

- Enabler activities refer to industries that support other sectors in decarbonizing. These include businesses providing renewable energy technologies, energy storage solutions, and smart grid technologies, which facilitate the shift towards a low-carbon economy across sectors

The Six Environmental Objectives

The EU Taxonomy focuses on six key environmental objectives. Each objective represents an area where economic activities must contribute to achieving sustainability:

- Climate Change Mitigation

- Activities that reduce or prevent greenhouse gas emissions fall under this objective. Examples include transitioning to renewable energy, improving energy efficiency, or enhancing carbon capture and storage technologies. This is essential for achieving the EU’s climate neutrality target by 2050.

- Climate Change Adaptation

- This objective focuses on activities that improve resilience to the impacts of climate change, such as rising sea levels, extreme weather, or temperature fluctuations. Examples include upgrading infrastructure to withstand floods or implementing heat-resistant crops in agriculture. These activities help mitigate the risks posed by an increasingly volatile climate.

- Sustainable Use and Protection of Water and Marine Resources

- Activities under this objective focus on responsible water management and the protection of marine ecosystems. This could include reducing water waste in industrial processes, preventing water pollution, or protecting marine biodiversity. Clean and sustainable water use is vital for both human health and ecosystem survival.

- Transition to a Circular Economy

- This objective aims to shift away from the “take, make, waste” model and promote resource efficiency, waste reduction, and recycling. Activities that foster the reuse of materials, increase product lifespan, or improve waste management (such as recycling programs) contribute to the circular economy. The goal is to keep resources in circulation for as long as possible, minimizing waste and reducing the need for new materials.

- Pollution Prevention and Control

- This objective addresses activities aimed at reducing or eliminating pollution, whether in the air, water, or soil. For example, introducing technologies that reduce industrial emissions or implementing more stringent waste treatment processes would fall under this category. The goal is to minimize harmful pollutants that can affect human health and natural ecosystems.

- Protection and Restoration of Biodiversity and Ecosystems

- This objective focuses on preserving and restoring biodiversity, natural habitats, and ecosystems. Activities may include reforestation projects, wildlife conservation, and efforts to rehabilitate degraded ecosystems. The preservation of biodiversity is critical for maintaining the balance of life on Earth and ensuring that ecosystems continue to provide essential services like pollination, water purification, and carbon sequestration.

The 4 delegated acts :

The EU Taxonomy is built on four key Delegated Acts, which set the foundation for assessing the sustainability of economic activities. These acts are evaluated through Technical Screening Criteria (TSC), which determine what qualifies as environmentally sustainable:

1. Climate Delegated Act (2021)

- Scope: This Delegated Act focuses on climate change mitigation and climate change adaptation objectives. It defines the criteria for economic activities that contribute to reducing greenhouse gas emissions and those that help adapt to the impacts of climate change.

- Key Sectors Covered: Renewable energy, energy efficiency, low-carbon transport, and climate-resilient infrastructure.

- Status: The Act entered into force in January 2022, and companies began using these criteria for reporting as of 2023().

2. Complementary Climate Delegated Act (2022)

- Scope: This Act extends the Climate Delegated Act by including criteria for nuclear energy and natural gas as transitional activities under certain strict conditions. These energy sources are recognized as contributing to climate change mitigation by helping transition away from more harmful fossil fuels.

- Key Sectors Covered: Nuclear energy, natural gas production, and energy distribution.

- Status: Entered into force in January 2023.

3. Environmental Delegated Act (2024)

- Scope: This Delegated Act covers the remaining four environmental objectives:

- Sustainable use and protection of water and marine resources.

- Transition to a circular economy.

- Pollution prevention and control.

- Protection and restoration of biodiversity and ecosystems.

- Key Sectors Covered: Water supply, waste management, construction, biodiversity conservation, and sustainable manufacturing processes.

- Status: Finalized and published in November 2023, with implementation starting from January 2024

4. Amendments to the Climate Delegated Act (2023)

- Scope: This act amends the existing Climate Delegated Act to include additional economic activities and update the TSC for climate change mitigation and adaptation.

- Key sectors: The amendments apply to sectors such as transport (including aviation and shipping), manufacturing, water supply, and disaster risk management.

- Objective: The changes include more ambitious TSC for sustainable aviation fuels (SAFs), fleet renewal, and promoting more sustainable practices in the aviation and shipping industries. It also updates activities related to manufacturing and infrastructure to reflect advances in low-carbon technology

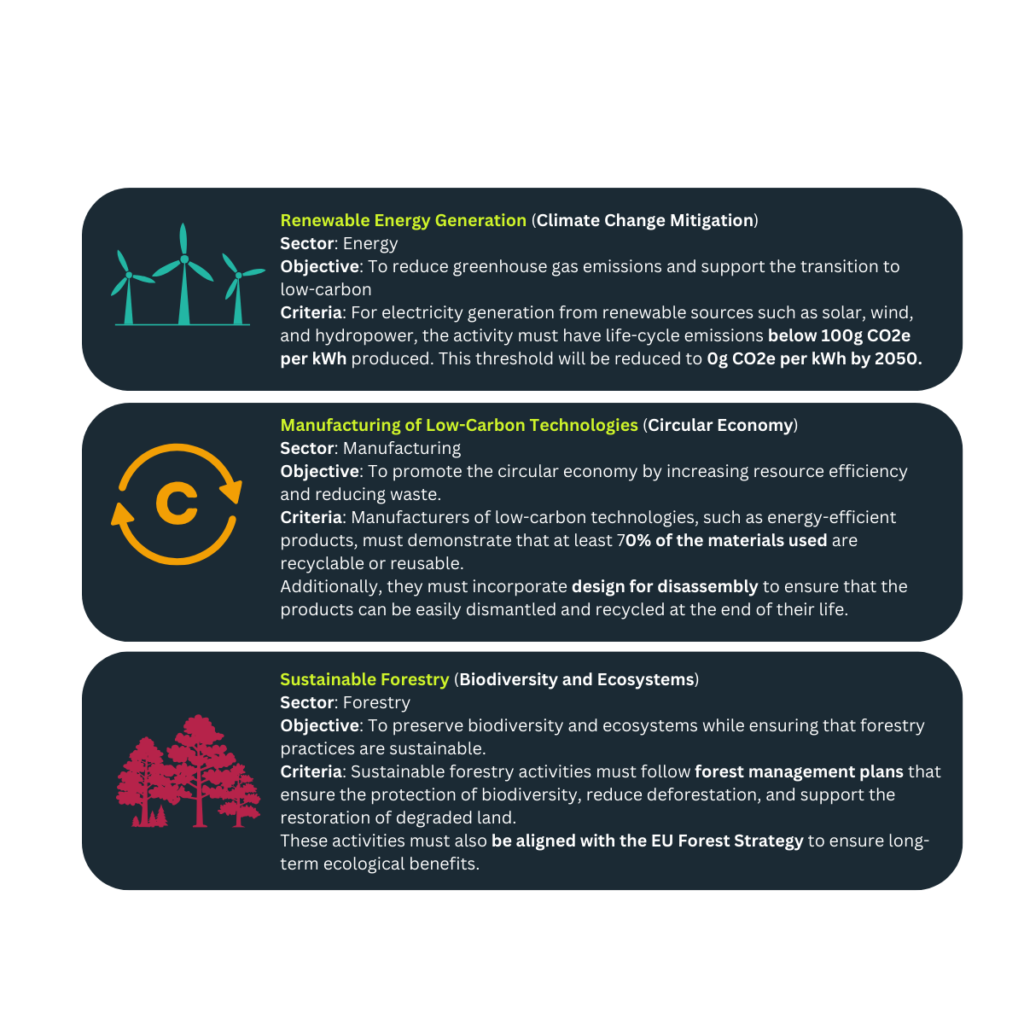

Technical Screening Criteria (TSC)

The Technical Screening Criteria (TSC) are essential components of the EU Taxonomy that define the standards and thresholds an economic activity must meet to qualify as environmentally sustainable. These criteria ensure that only activities that make a real, measurable contribution to environmental objectives are considered.

The TSC are detailed and vary by sector, providing specific metrics for each of the six environmental objectives. For instance, in climate change mitigation, a power generation activity must emit less than 100g of CO2e per kilowatt-hour (kWh) to qualify. This threshold will become stricter over time, encouraging industries to adopt cleaner technologies.

For circular economy activities, the TSC might specify a minimum percentage of recycled content in products or require that products are designed for repairability and recyclability. These criteria help promote the shift towards sustainable consumption and production.

The TSC serve as a technical benchmark, ensuring that all qualifying activities are contributing to the EU’s sustainability goals in a meaningful way. This creates consistency and credibility in how sustainability is measured across different sectors.

Reporting and Disclosure

To ensure transparency, the EU Taxonomy requires businesses and financial institutions to report how their activities align with the taxonomy. This includes detailing which percentage of their operations and investments are environmentally sustainable according to the Taxonomy criteria.

- Tools like the Taxonomy Compass and Taxonomy Calculator are available to help companies assess and measure their alignment with the EU Taxonomy framework. https://ec.europa.eu/sustainable-finance-taxonomy/home

- However, implementation is currently limited to large companies and financial institutions, meaning smaller companies are not yet subject to the same stringent requirements. As the directive expands, more businesses will be expected to comply.

2. For what impact and what’s Next for the EU Taxonomy?

Concrete Improvements Enabled by the Taxonomy

The EU Taxonomy has already started driving significant changes across various industries by setting clear standards for sustainability. Here are a few concrete examples of improvements made possible by the Taxonomy:

- Increased Investment in Renewable Energy: Thanks to the climate change mitigation criteria, projects in renewable energy—such as wind, solar, and hydropower—are receiving increased investments. Investors now have a clear framework for identifying which energy projects will have the most significant positive impact on reducing emissions, leading to a surge in capital directed toward renewable energy infrastructure.

- Shifting Industrial Practices in Heavy Manufacturing: Heavy industries, like steel and cement production, are notoriously difficult to decarbonize. The EU Taxonomy provides detailed guidelines for these sectors to adopt more sustainable production processes, such as using low-carbon technologies and carbon capture methods. This clarity has encouraged innovation and has begun to shift industrial practices toward more sustainable models.

- Advancing the Circular Economy in Consumer Goods: The Taxonomy’s circular economy criteria are pushing manufacturers of consumer goods—particularly in electronics and textiles—to rethink product design. Companies are now investing in more durable, repairable, and recyclable products. For example, smartphone manufacturers are developing models with modular designs to extend product lifecycles and reduce electronic waste, directly responding to Taxonomy standards.

- Preserving Water Resources in Agriculture: In agriculture, the Taxonomy’s emphasis on sustainable water use has led to innovations in irrigation and water management systems. Farmers are adopting technologies that reduce water waste and protect water quality, contributing to the preservation of critical water resources while ensuring long-term agricultural sustainability.

A Global Impact

The influence of the EU Taxonomy is not confined to Europe. As one of the most detailed frameworks for sustainable finance, it is setting the bar for global standards. Countries outside the EU are looking to the Taxonomy as a model for their own sustainability frameworks, particularly in regions like North America and Asia. This means that businesses operating globally will increasingly need to align with Taxonomy principles to maintain competitiveness in international markets.

The EU Taxonomy is also playing a key role in the development of international sustainable finance frameworks, such as the work being done by the International Platform on Sustainable Finance (IPSF). This global collaboration seeks to harmonize sustainable finance standards, and the EU’s leadership through the Taxonomy is helping shape a more unified approach to sustainability reporting and investment worldwide.

Driving Broader Regulatory Developments

The EU Taxonomy doesn’t stand alone—it serves as the foundation for a growing suite of sustainability-related regulations in the EU and beyond. Its comprehensive classification system is increasingly being used to guide other major regulatory frameworks aimed at environmental and social sustainability. By defining what is considered environmentally sustainable, the Taxonomy provides a blueprint for many other legislative initiatives.

Concrete examples of regulations influenced by the Taxonomy include:

- Corporate Sustainability Reporting Directive (CSRD): The CSRD, which requires companies to disclose more detailed information on their sustainability efforts, directly references the EU Taxonomy. It compels businesses to report how their economic activities align with the six environmental objectives. Thanks to the Taxonomy’s clear classification, companies can now provide more transparent and comparable sustainability disclosures.

- Ecodesign Sustainable Product regulation (ESPR): The ESPR will require companies to make products that are eco-designed, facilitate the circularity of products and make public procurement greener. All of this is done by aligning with the Eu taxonomy.

- Sustainable Finance Disclosure Regulation (SFDR): The SFDR mandates financial market participants to disclose how they integrate sustainability risks in their decision-making processes. The EU Taxonomy is crucial in this, as it helps define which investments can be considered sustainable, giving investors the tools they need to make responsible choices.

- Green Bond Standard: The upcoming EU Green Bond Standard relies heavily on the EU Taxonomy to define what qualifies as green projects. By using the Taxonomy’s criteria, issuers of green bonds can ensure that the proceeds are allocated to activities that contribute to the EU’s environmental objectives, thus enhancing the credibility of green finance.

Phased Implementation and Expanding Scope

The EU Taxonomy is being rolled out in stages to ensure comprehensive and effective integration across all sectors. The first set of criteria, covering climate change mitigation and climate change adaptation, is already in force. The criteria for the remaining four environmental objectives—water and marine resource management, circular economy, pollution prevention, and biodiversity protection—are being set up for the first time this year.

But this is only the beginning. As new sectors and technologies emerge, the Taxonomy will be updated to include more activities, ensuring it remains relevant and future-proof. This dynamic nature makes the EU Taxonomy a living framework that evolves with global sustainability challenges and innovations.

Conclusion

The EU Taxonomy is a critical tool for directing capital towards projects that are genuinely sustainable. By providing a clear, standardized framework, it ensures that investments are aligned with the EU’s climate and environmental objectives. For businesses, aligning with the Taxonomy not only helps meet regulatory requirements but also attracts sustainable investment. For investors, it offers transparency and confidence that their capital is supporting a greener future.

As the world moves toward sustainability, understanding and integrating the EU Taxonomy into business and investment strategies will be essential for creating a thriving, resilient, and sustainable economy.