The CSRD has the ambition to become the new standard for sustainability reporting, aligning EU businesses with the EU net-zero goals.

CSRD: A Comprehensive Guide for Businesses

The Corporate Sustainability Reporting Directive (CSRD) is a major new European Union (EU) regulation that significantly expands the scope and depth of sustainability reporting for companies operating within the EU. Implemented as part of the broader European Green Deal and climate-neutrality goals, the CSRD is designed to improve corporate transparency on environmental, social, and governance (ESG) issues. As sustainability becomes a top priority for investors, governments, and consumers, understanding the CSRD and how to comply is crucial for businesses.

This article explores what the CSRD is, why it was created, how companies can comply, and its connections with other regulations. It also provides a dedicated section on the concept of double materiality—a core principle of the directive.

Find the PDF summary here.

Access the EU page related to CSRD here.

What is the CSRD?

The Corporate Sustainability Reporting Directive (CSRD), adopted in April 2021 by the European Commission, is designed to replace and enhance the existing Non-Financial Reporting Directive (NFRD). The CSRD mandates that companies report detailed information on how they manage social and environmental challenges. This directive covers a much broader range of companies than the NFRD, expanding both the scope and depth of required disclosures.

Key Features of CSRD:

- Broader Scope: The CSRD applies to all large companies (with over 250 employees, €40 million in turnover, or €20 million in assets) and listed SMEs (small and medium-sized enterprises) in the EU, increasing the number of companies required to report on sustainability.

- Standardized Reporting: The directive introduces detailed sustainability reporting standards developed by the European Financial Reporting Advisory Group (EFRAG), ensuring consistency and comparability.

- Third-Party Assurance: Companies will need to have their sustainability information independently verified by an accredited auditor, which adds credibility to their reports.

- Digitalization: CSRD mandates that companies make sustainability data available in digital format, aligning with the EU’s goal of enhancing data transparency.

Why Was the CSRD Introduced?

The CSRD was introduced to address several gaps in sustainability reporting:

- Lack of Consistency: Under the NFRD, companies had significant discretion in how they reported sustainability data, making it difficult for stakeholders to compare companies. The CSRD solves this by requiring standardized reporting.

- Increasing ESG Concerns: Stakeholders, especially investors, are increasingly concerned with ESG factors and want detailed, reliable information. The CSRD was created to meet these growing demands for transparency.

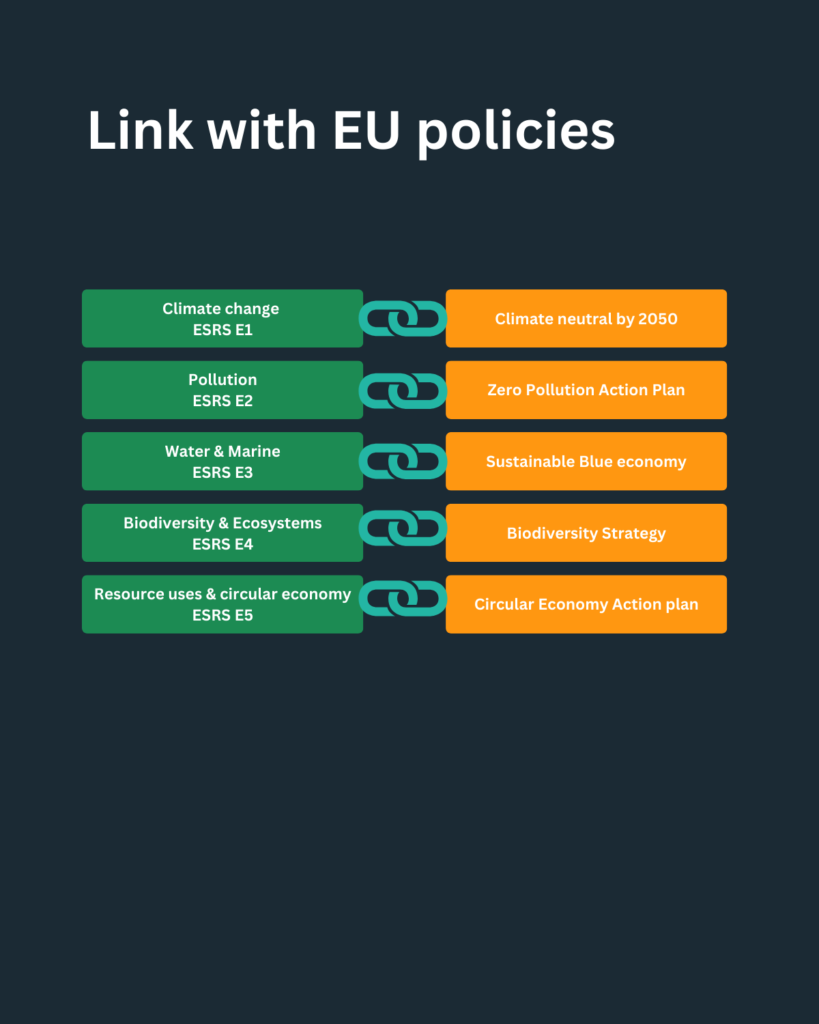

- Green Transition: The CSRD is a critical part of the European Green Deal, which aims to make the EU climate-neutral by 2050. By requiring companies to disclose their environmental impacts, the CSRD ensures that businesses contribute to the EU’s sustainability goals.

Specific Aims of CSRD:

- Strengthen Transparency: Enhance corporate transparency on ESG issues.

- Improve Decision-Making: Help investors, consumers, and other stakeholders make informed decisions based on reliable ESG data.

- Support the Green Transition: Align corporate strategies with the EU’s environmental objectives and global sustainability goals, such as the Paris Agreement.

How to Comply with CSRD?

Complying with the CSRD involves several steps, from understanding the reporting requirements to implementing internal processes and securing external audits. Here’s a guide to help companies comply with the CSRD:

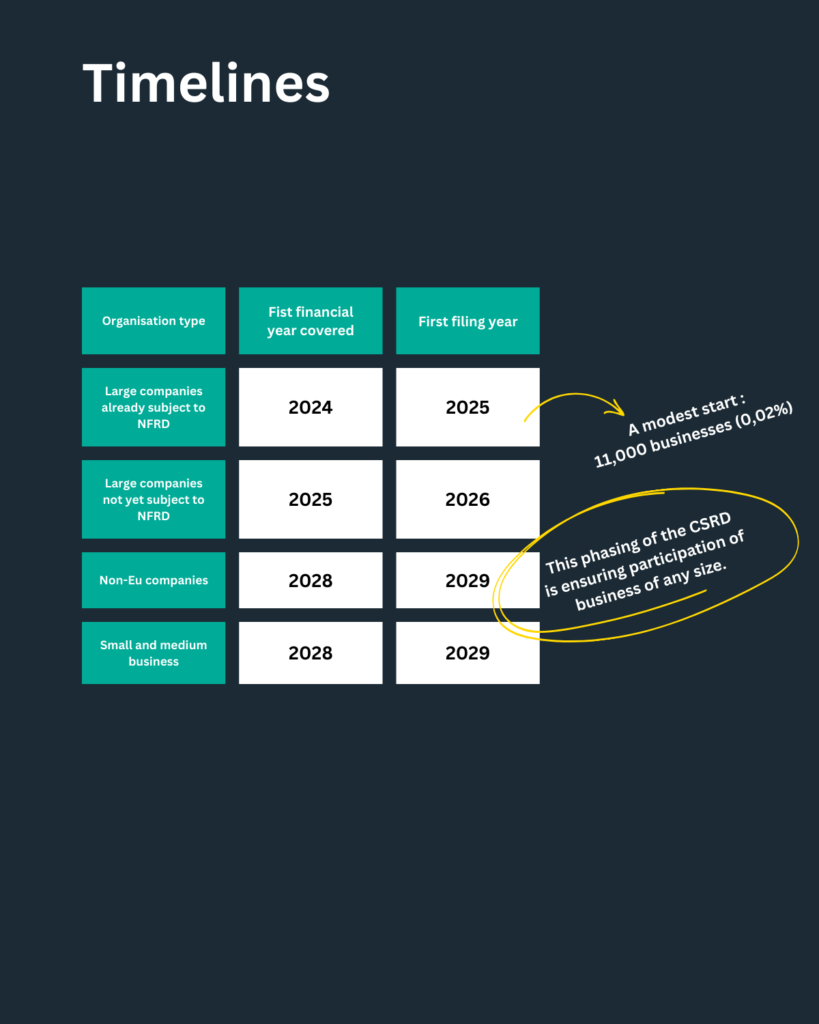

1. Determine Applicability:

- Companies must first determine whether they fall under the CSRD’s scope. If your company has more than 250 employees, €40 million in turnover, or €20 million in assets, or is a listed SME, you are required to report from the first year. Otherwise :

2. Understand the Reporting Requirements:

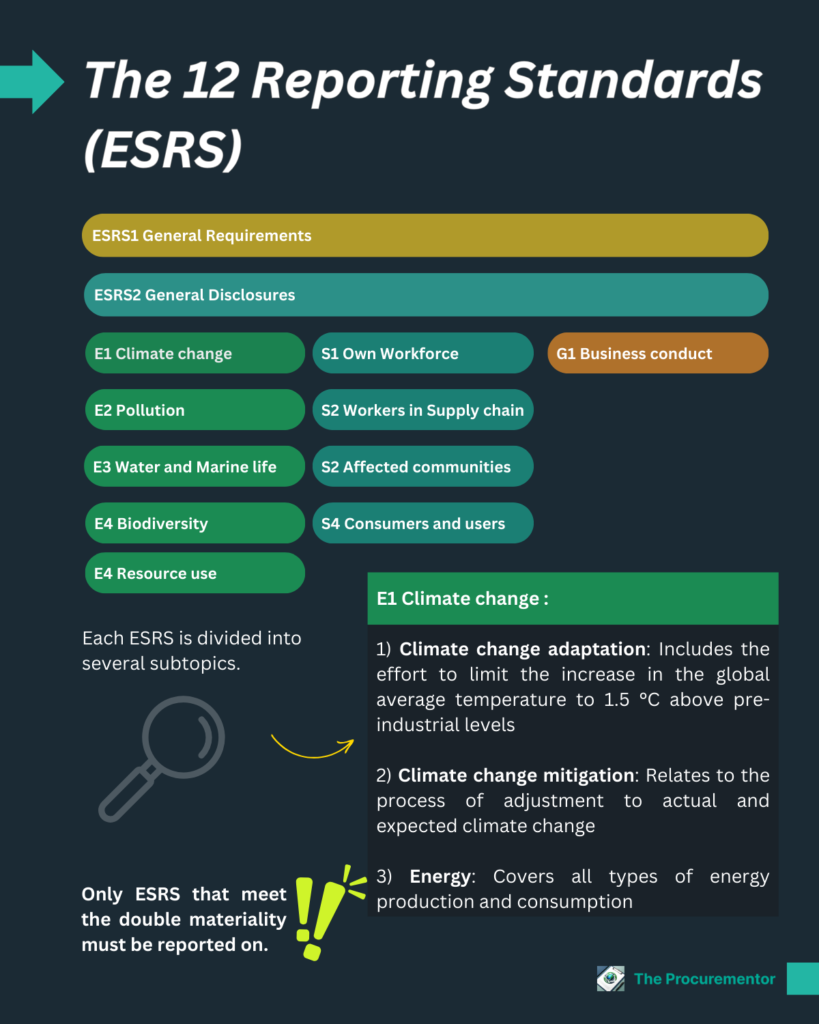

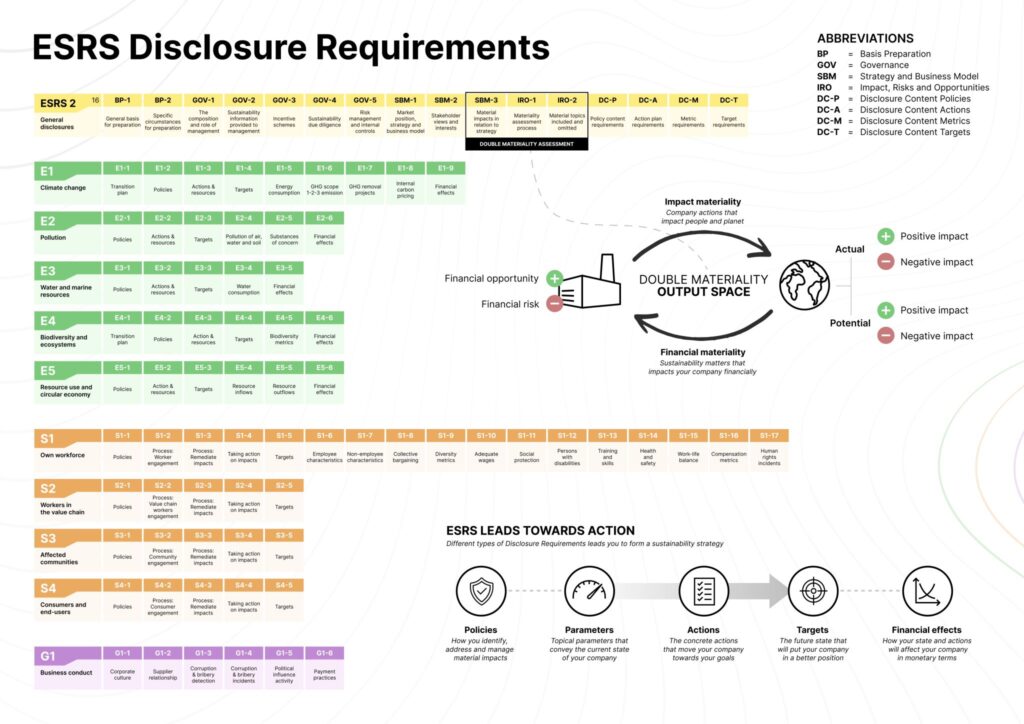

- Familiarize yourself with the reporting standards that are set by EFRAG. These standards cover a broad range of sustainability topics, including environmental impacts, social issues, and governance practices.

- The reporting is based on 12 ESRS :

3. Establish a Reporting Process:

- Companies must develop internal processes to collect and verify sustainability data. This involves collaboration across departments (e.g., finance, operations, human resources) to gather the required data.

4. Perform a Double Materiality Assessment:

- Double materiality is a key principle of the CSRD (explained in detail below). Businesses must assess their impact on the environment and society, as well as the financial risks they face from sustainability issues.

5. Ensure Third-Party Assurance:

- The CSRD requires that sustainability reports be audited by a third party. Companies must engage with accredited auditors to verify the accuracy of their sustainability data.

6. Digital Reporting:

- Prepare to submit your sustainability reports in a digital format as required by the European Single Electronic Format (ESEF). This aligns with the EU’s push for greater accessibility and transparency in sustainability data.

Double Materiality: A Core Principle of CSRD

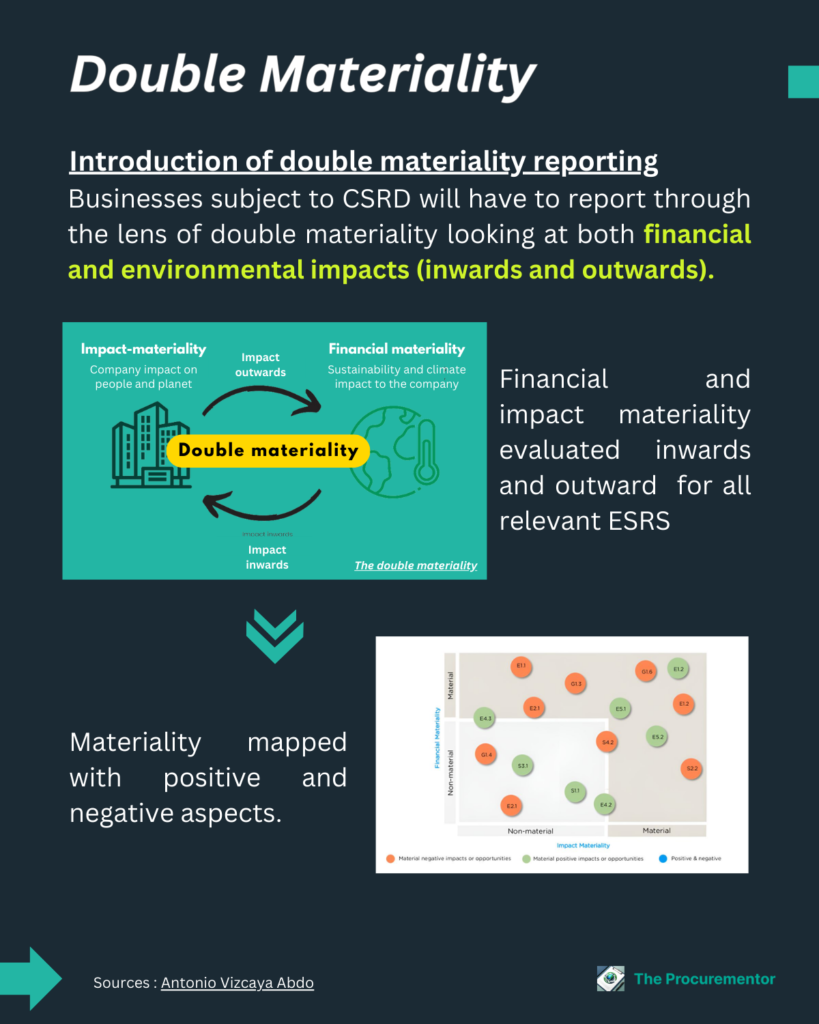

One of the most significant changes introduced by the CSRD is the concept of double materiality. Unlike traditional financial reporting, which focuses solely on how external factors impact a company’s financial performance, double materiality requires companies to report on:

- Financial Materiality: How sustainability issues affect the company’s financial performance and long-term resilience. For example, how climate change might affect a company’s operations, or how environmental regulations might impact profitability.

- Impact Materiality: How the company’s activities impact the environment and society. This includes emissions, resource usage, and social practices like labor conditions.

Why Double Materiality Matters:

- Holistic Reporting: Double materiality provides a more comprehensive view of a company’s sustainability performance, helping stakeholders understand both financial risks and the company’s broader environmental and social impacts.

- Forward-Thinking: By considering both financial and impact materiality, companies can anticipate future regulatory changes and align their strategies with long-term sustainability goals.

Example of Double Materiality in Action:

Example: Industrial Manufacturer (Steel & Semiconductor Chips)

Impact Materiality:

The company’s activities contribute to high carbon emissions from steel production and raise ethical concerns due to the environmental impact of mining rare earth metals for semiconductors. Waste generated from industrial processes can also harm local ecosystems.

Financial Materiality:

Rising costs from stricter emissions regulations on steel production could increase raw material expenses. Semiconductor shortages, driven by resource scarcity or supply chain disruptions, could delay production and raise prices. Both factors could hurt profitability. Additionally, not adopting sustainable practices may lead to fines or reduced investor confidence.

Ties to Other Regulations

The CSRD is closely linked with various EU and global regulations, ensuring that companies adopt a coherent approach to sustainability reporting. Key regulations that interact with the CSRD include:

1. EU Taxonomy Regulation:

- The EU Taxonomy provides a classification system that defines which economic activities can be considered environmentally sustainable. Companies reporting under the CSRD must disclose how their activities align with the EU Taxonomy.

2. Sustainable Finance Disclosure Regulation (SFDR):

- The SFDR requires asset managers and financial advisers to disclose how they integrate ESG factors into their investment strategies. The CSRD provides the necessary data for investors to comply with the SFDR.

3. Carbon Border Adjustment Mechanism (CBAM):

- The CBAM puts a price on carbon emissions associated with imported goods. Companies reporting under the CSRD must ensure that their supply chains are aligned with the EU’s carbon pricing mechanisms.

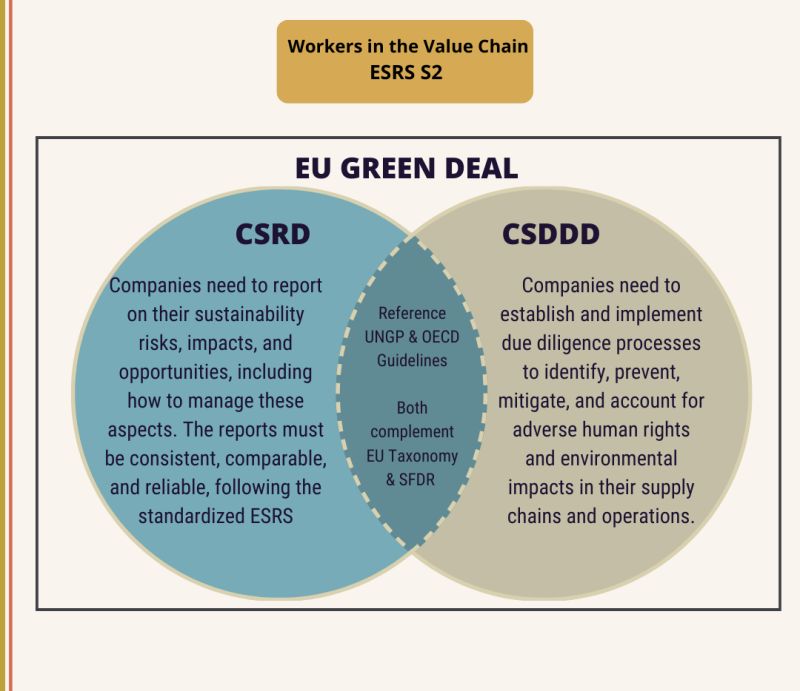

4. Corporate sustainability due diligence CSDD:

- The Corporate Sustainability Due Diligence Directive is a directive in European Union law to require due diligence for companies to prevent adverse human rights and environmental impacts in the company’s own operations and across their value chains and so intersect with the CSRD

5. Paris Agreement – EU green deal:

- The CSRD supports the EU’s commitment to the Paris Agreement by ensuring that businesses align with carbon reduction targets and other climate-related goals.

6. Global Comparability:

- Outside the EU, the CSRD aligns with global sustainability reporting standards such as those set by the Global Reporting Initiative (GRI) and the Sustainability Accounting Standards Board (SASB). This global harmonization allows multinational companies to streamline their reporting across different jurisdictions.

Benefits of the CSRD

The CSRD offers several advantages for businesses that comply, particularly in building long-term resilience and competitiveness. Key benefits include:

- Enhanced Transparency: With standardized reporting, companies can provide clearer and more reliable sustainability data to stakeholders.

- Investor Confidence: ESG investors rely on accurate sustainability data to make informed decisions. Compliance with the CSRD ensures that companies are more attractive to investors seeking sustainable opportunities.

- Reputation and Brand Value: Companies that lead in sustainability reporting can strengthen their brand reputation, attracting customers and partners who prioritize sustainability.

- Regulatory Compliance: As sustainability regulations tighten across the globe, the CSRD ensures that companies stay ahead of regulatory demands, avoiding penalties and legal risks.

Challenges of Complying with CSRD

Despite its benefits, the CSRD also presents challenges for businesses, particularly those that are new to sustainability reporting.

- Complexity of Reporting: The CSRD requires detailed and extensive disclosures, which may require significant time and resources to gather.

- Need for Cross-Department Collaboration: Compliance requires input from various departments, including finance, HR, operations, and sustainability teams.

- Third-Party Assurance Costs: Engaging an external auditor to verify sustainability data can be costly, especially for SMEs.

Conclusion

The CSRD represents a fundamental shift in corporate reporting, demanding that companies integrate sustainability at the core of their business operations. While the directive poses challenges, it also provides an opportunity for companies to build resilience, secure investments, and align with the global shift toward sustainability. Understanding the principles of double materiality and preparing for compliance will help businesses navigate this new regulatory landscape successfully.

By embracing sustainable procurement and reporting practices, companies can contribute to a greener, more equitable future while ensuring their own long-term profitability and compliance.

[…] The Corporate Sustainability Reporting Directive (CSRD) expands the requirements for corporate sustainability reporting, building on the previous Non-Financial Reporting Directive (NFRD). It mandates companies to report detailed information on their environmental, social, and governance (ESG) performance, with a strong focus on double materiality: how sustainability affects the company and how the company impacts society and the environment. […]